- Commodity Management & Trading

- Customer & Marketing Strategy

- Digital Engineering

- Station Studio

- Supply Chain & Industry 5.0

- Sustainability

Gas markets at a turning point

Gas remains a critical part of the energy mix. Even as the energy transition accelerates, it continues to support power generation, industrial activity and system flexibility, particularly in markets where renewable penetration is rising but dispatchable capacity is still needed. Gas is not disappearing from the system. What has changed is the market around it.

Prices respond more quickly and more sharply to geopolitical tensions, infrastructure disruptions and swings in global demand. Security of supply, once treated by many as a relatively stable assumption, has returned to the centre of strategic thinking. That matters because volatility does not stop at prices.

It also affects procurement choices, portfolio exposure, risk management and capital allocation. In a market where both physical flows and price signals can move fast, the challenge is not simply to secure supply. It is to preserve the ability to respond when the market changes.

No development has done more to reshape the commercial logic of gas than LNG. LNG has made gas more flexible and more global, but also more competitive and more exposed to international shocks. A market once anchored mainly in regional infrastructure now behaves much more like a globally traded system, shaped by route economics, cargo flexibility and competition between demand centres.

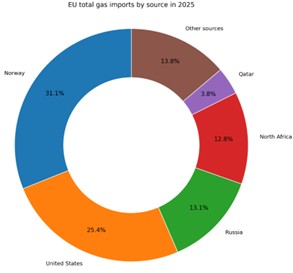

Europe offers the clearest example of that transformation. Since 2021, it has sharply reduced its dependence on Russian pipeline gas. According to the Council of the European Union, Russia’s share of EU pipeline gas imports fell from around 40% in 2021 to around 6% in 2025. In total EU gas imports in 2025, Norway accounted for 31.1%, the United States for 25.4%, Russia for 13.1%, North Africa for 12.8%, and Qatar for 3.8%.

The European Commission reported that in the first quarter of 2025, the United States represented 53% of LNG imported by the EU. Qatar remains an important structural LNG supplier, while Algeria has reinforced its role through pipeline deliveries into Europe. Together, these shifts have diversified Europe’s supply base and redrawn the map of gas flows into the region.

But Europe is only part of the story. Asia now sits at the centre of the global LNG balance. According to the IEA, emerging and developing Asian economies accounted for close to 40% of global gas demand growth in 2024, led by China and India. That is what makes LNG strategically different from pipeline gas: it links regional markets through global competition. When Asian demand strengthens, cargoes are pulled eastwards. When it softens, more LNG becomes available to Europe. LNG has, in effect, become the balancing mechanism of the global gas market.

This is why routes now matter as much as volumes. In the past, many market participants could focus primarily on source, contract and price.

Today, that is no longer enough. Cargoes can be redirected according to price spreads, terminal access, freight economics, weather conditions and shifts in regional demand. Europe and Asia increasingly compete for the same LNG cargoes, and developments in one basin can quickly affect availability and pricing in another. Understanding where gas is moving, and why, is becoming just as important as understanding where it is produced.

The next phase of market evolution is likely to reinforce that trend. The supply map is still being rewritten. New export capacity is set to come primarily from the United States and Qatar, while Canada has also entered the LNG export market through new Pacific Coast infrastructure. Russia continues to target LNG growth, even as sanctions and project constraints slow its progress. What matters is not only additional volume, but how new supply reshapes route options, basin competition and the relative weight of export hubs across the market.

For utilities, the implications are significant. Gas procurement is no longer simply about buying supply at the right price. It has become a broader portfolio management challenge that requires a more integrated understanding of optionality, logistics, market exposure and commercial risk. In this environment, fragmented processes are not just inefficient. They are a strategic weakness. When contract positions, logistics data, market signals and trading exposure sit across separate systems or teams, decision-making slows down precisely when speed and clarity matter most.

Better visibility does not simply improve reporting. It improves timing, coordination and the quality of commercial decisions. It also creates the foundation for more advanced capabilities:

- Market intelligence tools: they are evolving from traditional data repositories and EoD market price databases into real-time analytics, providing AIS vessel positioning, route analysis, destination and owner forecasting, tank level recognition… The opportunities doesn’t appear when the broker calls your door, but identifying the gap and providing a solution into the market.

- Demand Forecasting: legacy weekly planners and timeseries have evolved into sophisticated AI models, providing higher accuracy and being able to predict special situations based on weather conditions, price volatility, infrastructure outages…

- ETRM’s: most-known solutions are mainly focus on the post-trade processes, giving support to middle and back-office staff. Newest solutions are AI-assisted, providing tools to optimize routes and cargo allocations, run what-if scenarios to support the decision-making process, and improve the sourcing and nominations. Other key feature is the capability to calculate real-time risks and exposures. This enables to possibility to optimize the hedging from a static strategy-based back-to-back model into a new dynamic portfolio-level strategy.

- Algo-trading: in a fast-moving market, technology assisted order routing is becoming a must. Enable your trading desk to monitor prices, trigger events, define strategies (close the position, follow the price, procure an amount…) and monitor the execution in a reliable, audited and self-learning environment. Run your back-testing to check the performance of each strategy and move into AI-driven algos.

That is also where the future of gas trading is taking shape. The market is becoming more global, more data driven and more tightly linked to logistics than ever before. Competitive advantage will not come simply from access to supply.

It will come from the ability to connect market intelligence, route dynamics, portfolio exposure and execution in real time. In that sense, the future of gas trading is not only about molecules. It is about decision-making capability.

Real-time analytics, AIS vessel positioning, route análisis, destinatoin and owner forecatsing

Sophisticated AI models providing higher accuracy and prediction of special situations

Newest solutions AI-assisted, provinding tolos to optimize routes and cargo allocations, supporting the decision-making process

Enable your trading desk to move into AI-driven algos, technology assisted decisions

NTT DATA Insights